Nvidia (NVDA) has posted excellent Q3 earnings with an immense beat. Partially, it is thanks to the improvement in the price-performance metrics of its latest gaming GPUs, which have already sold out, at least in part due to acceleration in upgrade cycles. However, there are other factors at play which hearken back to dynamics seen in 2017-2018. Specifically, we have seen a repeat performance in the meteoric rise of Bitcoin (BTC-USD). Although there are more fundamental reasons for a Bitcoin price rally this time around as opposed to last time, with expectations of sustained stimulus devaluing the USD and highlighting the value in a fixed-supply currency, it has expanded Nvidia’s crypto end-markets again. Since there is a non-negligible risk of Bitcoin collapsing in 2021, there is also a risk of another Nvidia inventory glut. With perfect performance already priced into Nvidia, this could be enough to take Nvidia down by the double-digits and the tech-skewed market indices with it. Ultimately, the rotation into value could also be triggered, so investors should pay attention to sector diversification.

{kind=link}

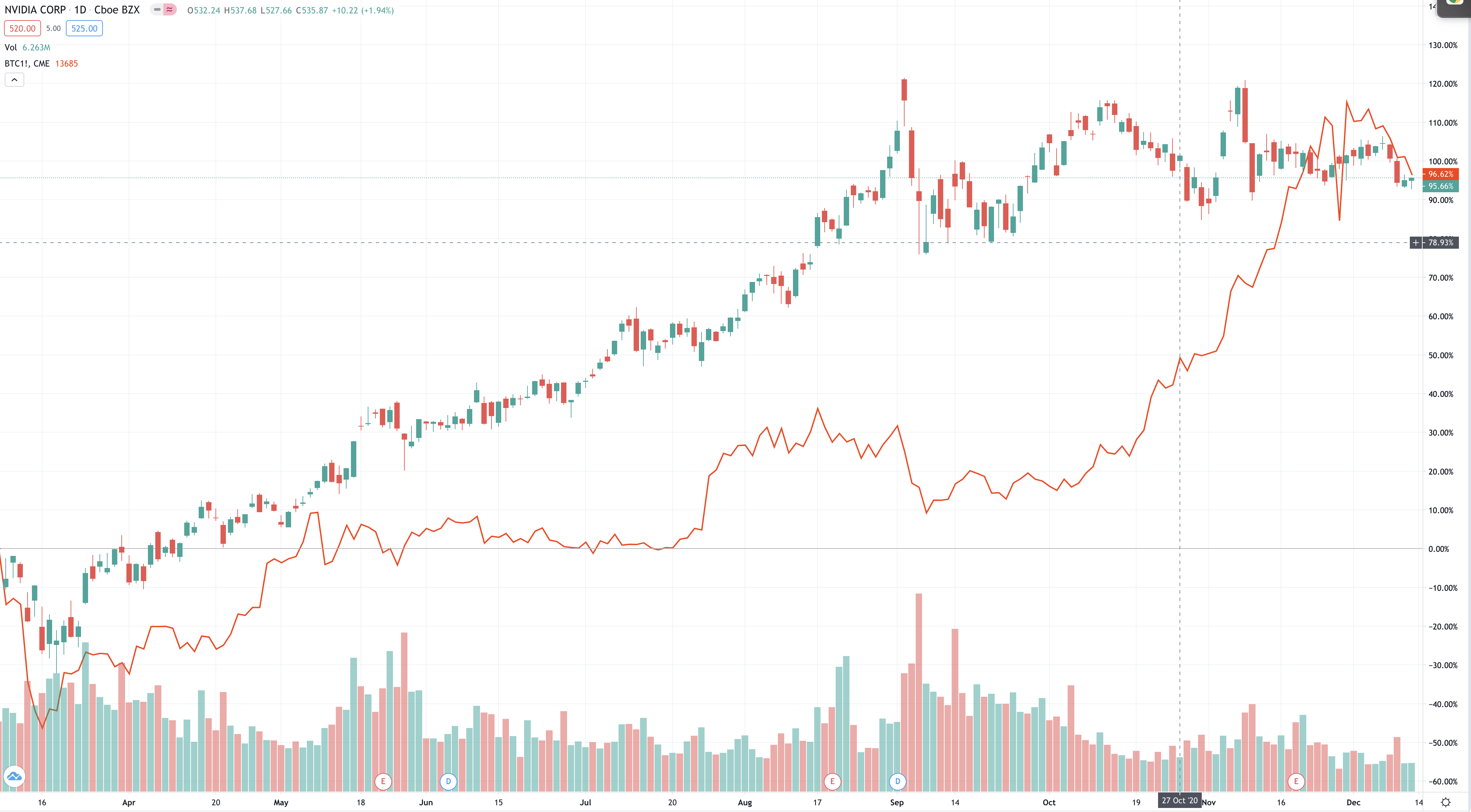

(Source: tradingview.com, comparing NVDA and BTC futures from March 2020)

Discussing Bitcoin’s Price

First of all, what lies behind the price of Bitcoin? Unlike last time, when Bitcoin’s trading was mainly driven by market greed, this time around there are more fundamental reasons for Bitcoin’s price growth. Primarily, the impact of COVID-19 on economies and the consequent stimulus actions taken by government is the reason why Bitcoin has seemed an attractive option compared to holding government controlled currencies. Many economies are taking the stimulus decision rather lightly, especially the US, where the only real contention around the stimulus was due to political noodling rather than properly voiced concerns around the budget deficit, which has become viewed as a hackneyed concern, irrelevant in the new economic order. However, it could still become a disaster, as it relies on foreign interest in holding US denominated bonds in order to continually finance it. If this were to change, the debt would become more costly, and the more demanding market could create issues in refinancing.

Although the probability of a real solvency problem is low, it will have to be paid for with high taxes and inflation down the road. Uncertainty around how much road we have till that becomes a problem would be the reason why Bitcoin has become more of an attractive asset. At the same time, the nature of the fundamental case has only really garnered it institutional interest as a marginal hedge for the failure of the new economic order. Indeed, most activity in the Bitcoin market is dominated by ‘professional’ bitcoin traders and retail investors, who would be holding Bitcoin as a disproportionately large portion of their portfolio to call it a marginal hedge. Moreover, gold also acts as a good hedge, and is a more trusted store of value. Although greater institutional interest could create a more robust market for Bitcoin, perhaps reducing its volatility, it makes some sense that the market cap of Bitcoin at around $350 billion is still a 30th of the market cap of all gold stocks, given continued regulatory concerns and a rather bad track record of trading. Indeed, the regulatory risks are massive, as states are not interested in relinquishing their extremely powerful monopoly on the currency, and have the power to really hamper access to crypto, including restricting investment as in some jurisdictions, which would severely affect institutional ability to hold those assets and would impact the upside case for Bitcoin and crypto in closing the gap on gold.

GPU Glut Risks

Regardless of the long-term future of Bitcoin, what is for sure is that of this moment, the value of mining assets, including GPUs has gone substantially up. In 2018, after the crash of Bitcoin at the turn of the year, we started to see the impacts on Nvidia’s financials that a collapse in crypto-related revenue could have. Reports came out about inventory gluts due to severe miscalculations by the company on the longevity of crypto demand. These reports eventually became vindicated in coming quarters when Nvidia seriously underperformed and lost 50% of its value. With Nvidia now up 60% from the highs of that period, the price could become even more sensitive to an overvaluation of the crypto exposure. With new generation GPUs sold out, and in the process of restocking, production decisions taken by Nvidia to capitalize on newfound crypto demand could easily result in a similar situation to last time if expectations are not properly managed in investor communications. Inventory gluts are very ugly on company financials, as it impacts both income and cash flow metrics, and can last a long time if GPUs valued by gamers were to hit the second-hand markets in large quantities, depressing new GPU sales.

Although gluts are ultimately temporary, especially for high-value products like GPUs, the impact on Nvidia’s share price could end up becoming substantial enough to cause the chain selling that we are all too familiar with in algorithmic and sentiment dominated markets. With the rise in NVDA rather proportionate to the rise in BTC, we are worried about the potential of a pullback. Although it is uncertain, as Nvidia is not able to disclose the entirety of its crypto-related revenue due to some of it being baked into gaming, we think that revenues could easily represent up to 10% of Nvidia’s revenue line, perhaps even 15% as was calculated in the last crypto boom. Indeed, much of the beat this quarter of $700 million might be attributed to better than expected crypto demand, which can be explained by the fact that management wasn’t guiding for it and analysts have a hard time estimating it. If you extrapolate that figure for another quarter or more depending on the performance of cryptocurrencies, the 15% figure becomes very feasible. Naturally, the disappearance of 15% of revenue due to a Bitcoin collapse is a risk that investors should take seriously, as it will certainly dent if not crumple the share price.

Takeaways

I am not speculating that Bitcoin and crypto in general are going one way or another. I think its current price levels are more justified this time around than last time, but I don’t think anything has really shifted the paradigm on Bitcoin yet. For that, widespread regulatory approval, while keeping crypto viable, would have to occur. When/if that will happen is anyone’s guess. The real takeaways concern investors and traders in Nvidia, which are that the price of the stock in the short to medium-term is going to be at least somewhat governed by cryptocurrencies, and any problems in those markets will eventually become a problem in Nvidia’s even if with a quarter or two of lag. To stockholders generally, the takeaway is that there is yet another systematic risk that needs to be considered related to, but not exclusive to, the macroeconomic situation. By impacting the business dynamics of one of the more cited, interesting and larger-cap tech names, in a market environment ultimately characterized by uncertainty and sensitivity to adverse events, problems for Nvidia at the wrong moment could amplify volatility in the markets, and could even trigger the anticipated value rotation. To be safe, we think it’s time to position more aggressively into industrials and real assets to diversify exposures away from the tech space, and attention should be paid to the fact that indices remain weighted heavily towards tech.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Not investment advice. We are not registered investors.