Last week, we concluded Part 1 with the observation that the most disruptive aspect of digital transformation is perhaps its implications on the concept of money. With an expanding platform, Bitcoins, Ethereum, and Ripple threaten to challenge fiat money, that which is issued by the different countries’ central banks.

Do these digital assets have what it takes to be accorded the same trust as fiat money to fully serve society?

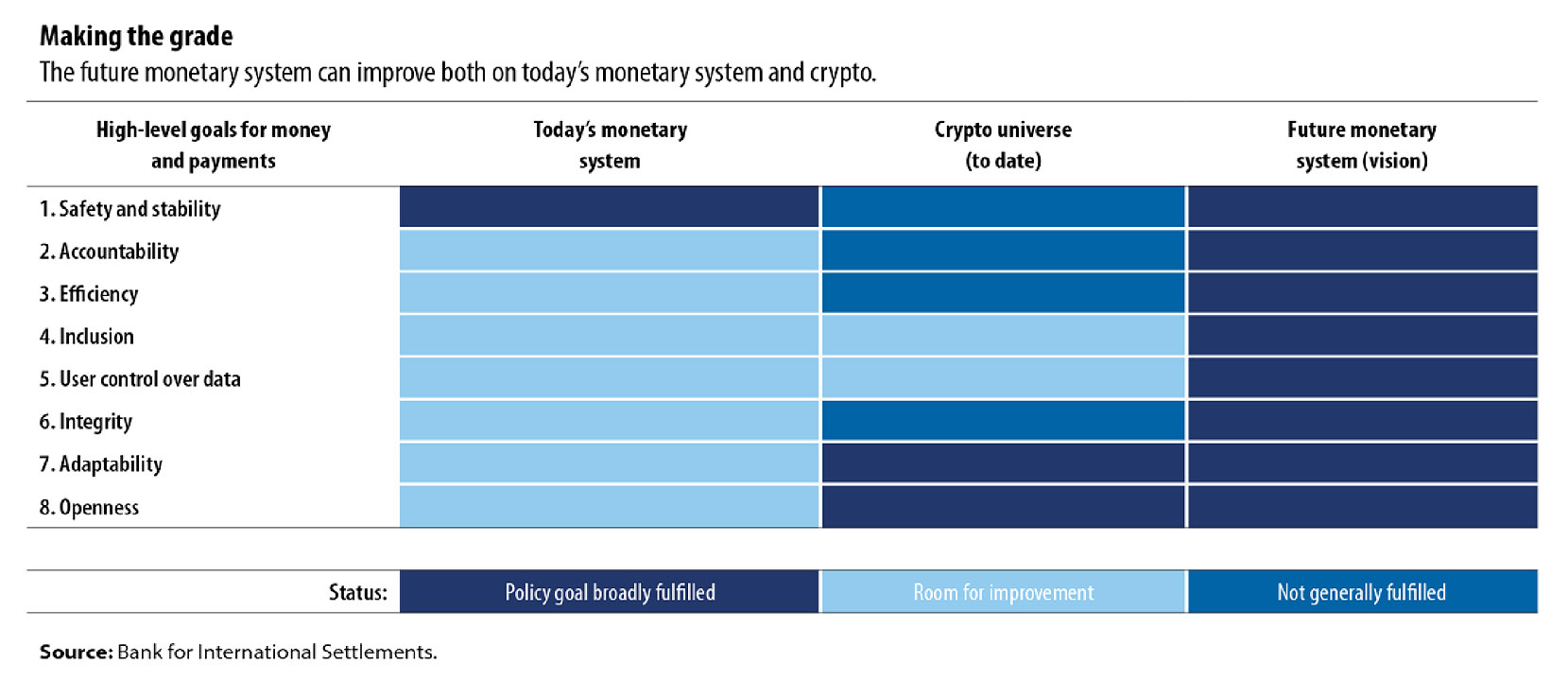

The literature is one in saying that security and stability are important features of a money pretender, whether public or private, who should be accountable to the general public. As Agustin Carstens, Jon Frost, and Hyun Song Shin of the Bank for International Settlements (BIS) argued in IMF’s Finance and Development of September 2022, a money pretender must also be efficient and inclusive with participants having control over their data. Fraud and abuse are ringfenced. To be global, it would have to be supportive of cross-border transactions.

Carstens, Frost, and Hyun were rather categorical that “today’s monetary system is generally safe and stable, but there is room for improvement in many areas.”

To transition from what we have today to a future monetary system with stronger accountability, efficiency, inclusion, user control over data, integrity, adaptability, and openness, the so-called crypto universe may be harnessed for its adaptability and openness for cross border transactions.

As to the rest of its functionalities, the crypto universe is claimed to be structurally flawed. The BIS argued that first, it possesses no nominal anchor as it makes use of crypto currencies and the so-called stablecoins which, in turn, piggyback on a sovereign currency such as the US dollar, or an exchange-traded commodity like precious metals. And here’s the rub from BIS: crypto currencies are not currencies while stablecoins are not stable. The BIS cited the reported implosion of TerraUSD last May while the markets continue to question the backing of the largest stablecoins, Tether.

In short, “stablecoins seek to ‘borrow’ credibility from real money issued by central banks.” BIS was fully justified to say that if central bank money did not exist, somebody would have to invent it to make crypto universe somewhat viable.

Second, the crypto system motivates fragmentation. BIS correctly pointed out that indeed money is a matter of social convention, that its wide use further propagates itself as a store of value and a medium of exchange, that this popular acceptability is hinged on the fact that its stability, safety, and finality of settlement are all guaranteed by a trusted institution like the central bank.

In the absence of such a central entity, and crypto’s decentralized nature given its reliance on anonymous transactors to confirm consummation by payment of fees and charges, congestion is unavoidable. Incentives have to be substantially scaled up, even as that could effectively disincentivize its wider use. With higher cost, nothing prevents the transactors from shifting to other blockchains resulting in fragmentation.

Therein lies crypto’s shortcoming. Its stability and efficiency may be subject to question and doubt. Unregulated, the crypto universe is driven by participants without established accountability to the general public. And in view of reported incidents of fraud, theft, and various scams in recent years, we share the BIS’s concern about market integrity.

For this reason, Monetary Authority of Singapore’s (MAS) Ravi Menon, in the same IMF publication, called for caution against any delay in facing the challenges of crypto innovations. “Central banks and regulators cannot afford to wait for clarity on how crypto-related innovations will shape the future of money and finance.” They are sweeping the financial landscape with great momentum.

MAS recognizes the great potential of digital assets in enabling more efficient payment transactions. MAS related that in the areas of cross border trade and settlement, trade finance and capital market activities, using blockchains could reduce settlement time from a few days to less than 10 minutes and trim cost from 6% to less than 1% of transfer value. In trade finance, the processing time for letters of credit has been shortened from five to 10 days to less than 24 hours. In capital market transactions, clearing and settlement of securities transactions have been reduced from two days to less than 30 minutes. In other business areas, digital transformations in Singapore have allowed automatic execution of say, coupon payout, whenever pre-set conditions are met.

However, like the BIS, MAS argued that privately issued cryptocurrencies fail as money — or as a medium of exchange, a store of value, or as a unit of account. They are no more than tokens of blockchain projects but because “they are actively traded and heavily speculated on, with prices that are divorced from any underlying economic value on the blockchain,” they could not pretend to be either tokenized currency or investment asset. To MAS, stablecoins have better potential provided they are appropriately regulated and supported by good reserves to which they are tied. But such linkage could also pose risks to stablecoins. When liquidity issues strike, stablecoins may have to sell at a loss.

Which brings us to Cornell University’s Eswar Prasad who pointed out in the same IMF publication that a payment infrastructure that is exclusively private sector-driven might be efficient and cheap, as cryptos and stablecoins, but “some parts of it could freeze up in the event of a loss of confidence during a period of financial turmoil.”

This means, if digital currencies should dominate the payments and settlements landscape, and stability and trust become an issue, it is possible for a modern economy to literally freeze. Prasad pointed out that if only to prevent this impasse, central banks should consider issuing digital forms of central bank money for retail payments, or central bank digital currencies (CBDCs). Should private money fail, central bank currency could very well offer a public payment option. It could also help promote financial inclusion as well as increase efficiency and stability of the payments system. CBDCs could prevent illegal activities like drug deals, money laundering, and terrorist financing. More and more financial activities could be flushed out from the gray market and move them to the formal economy.

CBDCs have their weaknesses as well. If the banking public decides to patronize CBDCs instead of keeping their money in regular bank accounts, the commercial banking system would be starved of their major source of loanable funds. Central banks might end up allocating credit and, in the process, discouraging digital innovation. In addition, CBDCs could lead to loss of privacy. Currency-issuing central banks would always wish to ensure that its digital currency is used only above board.

Most important, central banks should be able to formulate correct monetary policy as lending platforms continue to go digital, reducing the role of commercial banks in financial intermediation. More research is necessary to pin down how monetary policy transmission would evolve and affect even the nature of money without affecting its ability to promote price stability and sustainable economic growth.

Prasad’s concluding points are sobering: “Financial innovations will generate new and as yet unknown risks, especially if market participants and regulators put undue faith in technology.” A decentralized and fragmented payment system works well in good times when market confidence is not so much of an issue. During bad times, confidence could sink, especially when digital currencies are not backed by reserve assets.

Thus, as the BIS stressed, central banks remain indispensable in leveraging on both digital transformation and its role as monetary authority in fostering such a core of trust in the market. The markets are confident that in general, central banks would do their job as issuers of sovereign currency, providers of the ultimate payments infrastructure, and regulators and supervisors of financial services and their instrumentalities.

The Philippines’ Bangko Sentral ng Pilipinas may not find as yet the imperative of issuing CBDCs given the generally well-functioning payment systems and adherence to the broad principles of financial inclusion. What is urgent perhaps is to begin constructing a technology infrastructure that would enable the issuance of retail CBDCs should it be necessary, especially when conditions call for it.

It is not farfetched for the digital asset ecosystem to evolve as a fixture in the Philippine financial system, even alongside the regular bank intermediation system. But judicious preparatory work in developing frameworks that seek to balance risks and opportunities offered by digital transformation is the only way to a brave new digital world.* n

* For instance, MAS has launched an initiative, Project Guardian, to consider possible digital asset applications in wholesale funding markets. DBS Bank, JP Morgan, and Marketnode are leading this project that involves creating a liquidity pool of tokenized bonds and deposits locked in a series of so-called smart contracts. This is aimed at achieving seamless secured borrowing and lending of these tokenized bonds through the smart contracts.

Diwa C. Guinigundo is the former deputy governor for the Monetary and Economics Sector, the Bangko Sentral ng Pilipinas (BSP). He served the BSP for 41 years. In 2001-2003, he was alternate executive director at the International Monetary Fund in Washington, DC. He is the senior pastor of the Fullness of Christ International Ministries in Mandaluyong.