Throughout history, people have attempted to create something from nothing.

On one hand, there are real scientific innovations- new developments that allow us to tap into denser energy sources and increase productivity to improve most peoples’ quality of life.

They create something from nothing only in the sense that they make resources go a lot further than they used to, and make it easier to access more resources. They organize matter, information, and human activity better than prior innovations. In other words, if you were to show a caveman a smartphone, he’d think of it as magic.

On the other hand, there are attempts at things like alchemy and perpetual motion machines– approaches that misunderstand science. Even someone as famously smart as Isaac Newton spent quite a bit of time studying alchemy. It’s an easy trap to fall into.

Large swaths of the cryptocurrency market are basically the modern version of alchemy. While there are real innovations in the space, such as bitcoin, fiat-collateralized stablecoins, and a number of experimental technologies, there is also a huge amount of speculation, pump-and-dump schemes, technological claims that obfuscate the trade-offs and risks they are taking, and so forth.

This article is a post-mortem analysis of the multi-billion dollar failure of Terra (LUNA-USD), which is a cryptocurrency network based around an algorithmic stablecoin.

Riding the Coattails of Bitcoin

Before starting at the SEC, I had the honor of researching, writing, and teaching about the intersection of finance and technology at the Massachusetts Institute of Technology. This included courses on crypto finance, blockchain technology, and money.

In that work, I came to believe that, though there was a lot of hype masquerading as reality in the crypto field, Nakamoto’s innovation is real. Further, it has been and could continue to be a catalyst for change in the fields of finance and money.

At its core, Nakamoto was trying to create a private form of money with no central intermediary, such as a central bank or commercial banks.

– Gary Gensler, SEC Chairman, August 2021

Local payments have historically been a private and physical process. I hand you physical cash, and you hand me the goods. It’s hard to surveil or prevent that type of transaction.

But for years, people relied on large centralized intermediaries (commercial banks and central banks) if they needed to send payments further distances.

If I wanted to send money to my friend in Chicago, or especially to my other friend in Tokyo, or buy something from a merchant in those cities, I needed to go through a big bank. In one of various ways, I would tell my bank to send their bank money, and if it goes internationally, it would ultimately involve our countries’ central banks too.

As an American, and for those types of destinations, going through centralized entities for long-distance payments has not been a big deal, because they don’t block my payments. They are expensive and slow, though.

But for the majority of people in the world with restrictive monetary regimes and persistently high inflation (over half the world lives in an environment of authoritarianism and/or recurring double-digit inflation), the lack of alternatives has been restrictive. For developed market journalists and academics and analysts to not realize this, is a form of privilege that many of them are unaware of.

The invention of Bitcoin (BTC-USD) changed this reliance on centralized intermediaries, because it brought the first credible type of self-custodial peer-to-peer money. Anyone with an internet connection could send liquid value to anyone else in the world with an internet connection, without relying on commercial banks or central banks. Nobody has to hold their money for them, and they don’t have to ask permission from any centralized entity to send that value to someone else. I explored this concept in my article, What is Money, Anyway?

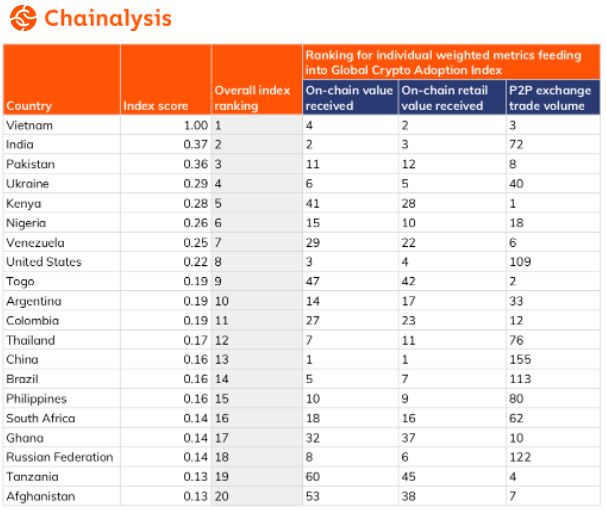

It’s perhaps unsurprising, then, that 19 out of 20 of the leading countries in the Chainalysis Crypto Adoption Index are developing countries. In general, people in these countries deal with lower levels of property rights, lower levels of financial freedom, and higher levels of currency inflation, than most readers of this article do:

Chainalysis

Bitcoin became the fastest asset in history to touch $1 trillion market capitalization, and has recovered from three 80%+ crashes and several 50%+ crashes to keep reaching new highs:

Look Into Bitcoin

Bitcoin holders have to put up with volatility, technical risk, and other things like that, but what was offered in a technical sense is truly new, regardless of what ultimately happens with the network in the long run. The protocol uses energy and open source code to establish a publicly-auditable global consensus ledger, rather than relying on human decisions to come to that consensus.

But after bitcoin, came twenty thousand imitators.

Some of them increase node requirements, and therefore sacrifice decentralization, to increase transaction throughput (thus defeating the purpose of a blockchain).

Some of them take out the energy input and replace it with a human governance input, which again reduces decentralization in various ways.

Some of them take on additional complexity in order to achieve more code expressivity, which also increases node requirements and reduces their decentralization.

Basically, there’s a theme here. It’s decentralization that keeps getting thrown under the bus with each new “innovation” from competing projects.

Satoshi Nakamoto purposely sacrificed most metrics in his bitcoin design in order to achieve an automated, decentralized, and auditable global transfer agent and registrar, and nothing else. He combined existing technologies like Merkle trees and proof-of-work algorithms and then added difficulty adjustments to the mix, and this combination was his innovation.

Proof of work is not only useful but absolutely essential. Trustless digital money can’t work without it. You always need an anchor to the physical realm. Without this anchor, a truthful history that is self-evident is impossible. Energy is the only anchor we have.

Proof of work = trust physics to determine what happened.

Proof of stake = trust humans to determine what happened.

Bitcoin has been updated by developers via soft forks (backward-compatible opt-in upgrades) a number of times since then, but the core design remains unchanged. It’s had 99.98% uptime since inception, and 100% uptime since March 2013.

Not even Fedwire, the US Federal Reserve’s interbank settlement system, has had 100% uptime during that period.

Most other cryptocurrency designs claw back some of that decentralization, reliability, and security to add back more features, and then advertise this to investors as innovation.

And around the margins, there are indeed some innovations. For example, a federated database and computation layer can be a useful thing. But for the most part, the space is filled with misunderstandings of what it is that Nakamoto created, and why.

These trade-offs are rarely advertised to investors (and sometimes not understood by the founders), but rather are marketed as though they are pure technological improvements. And that advertising draws a lot of people in, especially when combined with VC-funded temporary economic incentives.

Unlike the bitcoin network, which has no central organization to market for it, most of these other projects have central foundations or persons that play a critical role in the marketing and ongoing operation of the network.

People working in the bitcoin ecosystem have often been critical of these other protocols. From an outside perspective, the whole “crypto” ecosystem may seem homogenous, but within the industry, it’s not really that way. People working on these “altcoins” as they are called have a natural incentive to try to associate with bitcoin but to market various reasons why their token is better, while bitcoin proponents have a natural incentive to point out all of the risks and trade-offs that these other cryptocurrencies are making when they’re claiming to be innovative.

Satoshi Nakamoto put out the open-source software, updated it for a couple of years in the beginning, never gave himself a pre-mined amount of bitcoins, never spent any of his mined bitcoins, and then disappeared to let others carry forward his project.

The network has relied on a rolling set of open source developers ever since, with no leader. There’s nobody who can push updates onto users. There’s nobody to turn to when the price goes down and ask what they’re going to do about it. Bitcoin never raised capital, doesn’t pass the Howey test, and therefore is not a security; it’s categorized as a digital commodity for most purposes.

In contrast, many other protocol developers have gotten rich off of their creations by giving themselves significant pre-mined coins, and continue to operate their networks in a centralized way, while marketing them as being decentralized. Many of these coins/organizations raised capital, pass the Howey test, and therefore have many characteristics of securities.

If they were fully honest with their designs, they would be like startup companies, and we could analyze them as such. But in a practical sense, many of them are basically unregistered securities, operating in a global gray zone before regulators figure out how to catch up while advertising themselves as being decentralized networks.

That’s not to say that all crypto is bad or without technological contributions, but it’s to say that the overall industry is quite full of scams, frauds, and well-meaning but ultimately doomed projects, as a percentage of what has been created. Bitcoin left a big wake in its path, and sharks have been happy to fill that wake and figure out how to make a lot of money quickly.

For the most part, it’s like bitcoin is the iPhone of this industry, and then there are thousands of cheap knock-off buggy phones, with Apple logos glued onto them, being marketed to people as well. Investors need to be very cautious if they choose to speculate in various crypto projects.

Several exchanges in the industry fuel bubbles for a quick buck as well. If something starts to get momentum, including meme coins like Dogecoin (DOGE-USD) or Shiba Inu (SHIB-USD) that don’t realistically have a substantial future, they promote those coins to their users, which can suck retail investors into buying the bubble top. Plus, a lot of YouTube and TikTok influencers pump small coins and use their audience as exit liquidity.

Terra: “The Central Bank That Wasn’t”

Terra is a cryptocurrency network based around an algorithmic stablecoin called TerraUSD (UST-USD) and uses its native token, Luna (LUNA-USD) as basically its equity capital. A create/destroy mechanistic relationship between the two is what is meant to keep the peg stable.

It marketed itself as being decentralized, but ultimately it was not:

Terra Homepage

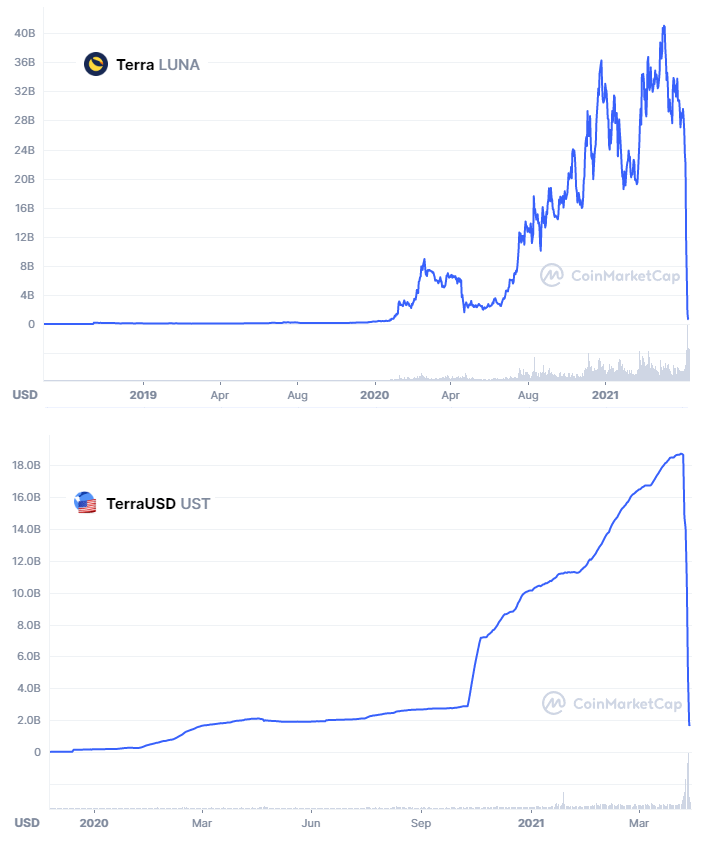

At its peak, Luna had a $40 billion market capitalization and TerraUSD had a nearly $20 billion market capitalization. It was heavily invested in by crypto VCs and retail investors. Much of this is now wiped out. The TerraUSD peg broke, and Luna equity was eviscerated. This happened from May 7th to May 12th primarily and is still an ongoing saga.

Coin Market Cap

When the Terra ecosystem was small, I mostly ignored it. I keep an eye on various crypto projects once they reach the top 20 by market capitalization or so, to have an idea of what they are doing, but can only keep track of so many things.

By mid-March 2022, the Luna Foundation Guard was created to try to shore up the Terra/Luna ecosystem, and they began purchasing bitcoin, which was intended to serve as another line of defense for Luna’s token equity. That’s when I started to dig deeper into their ecosystem to analyze the risk.

For months, a number of people in the bitcoin ecosystem were warning about Terra. Industry professionals including Brad Mills, Nic Carter, Cory Klippsten, and many more people than I can name here were publicly critical of it. Cory Klippsten in particular was loudly and repeatedly warning people about it.

I analyzed the situation, read several of the critical views of the project, and then went and read counter-arguments from the Luna bulls about why those risks were supposedly unfounded. And my view was that the risks were pretty clear and accurate. It’s not really a technical risk; it’s an economic risk based on unstable economic design and unsustainable financial incentives.

Rather than re-write my full analysis, I’ll share what I wrote for Stock Waves subscribers on April 3, 2022:

Luna Defense Guard Bitcoin Accumulation

Some of this recent bitcoin breakout was probably due to over $1.3 billion worth of bitcoin purchases by the Luna Foundation Guard, which plans to buy $3 billion in bitcoin for reserves and to eventually increase that reserve to over $10 billion.

I’ll rewind a bit and explain what the heck that means.

Terra is a proof-of-stake smart contract cryptocurrency based around algorithmic stablecoins, and particularly around TerraUSD or “UST” which is their dollar stablecoin. Unlike USDT or USDC, which are custodial stablecoins (where centralized entities hold fiat dollars as assets and issue redeemable stablecoin tokens representing those assets), UST is an algorithmic stablecoin. This means that it approximates the value of a U.S. dollar but does not hold U.S. dollars.

The way this works is that Terra’s primary token, LUNA, serves as the volatility offset for UST. If UST goes above $1, there is an arbitrage opportunity to burn LUNA and create more UST. If UST goes below $1, there is an arbitrage opportunity to create LUNA and burn UST. UST is supposed to remain around $1, while LUNA is allowed to be volatile. The more demand there is for UST over time, the higher UST and LUNA market cap should go. It’s like a central bank that tries to incentivize market participants to do both sides of open market operations.

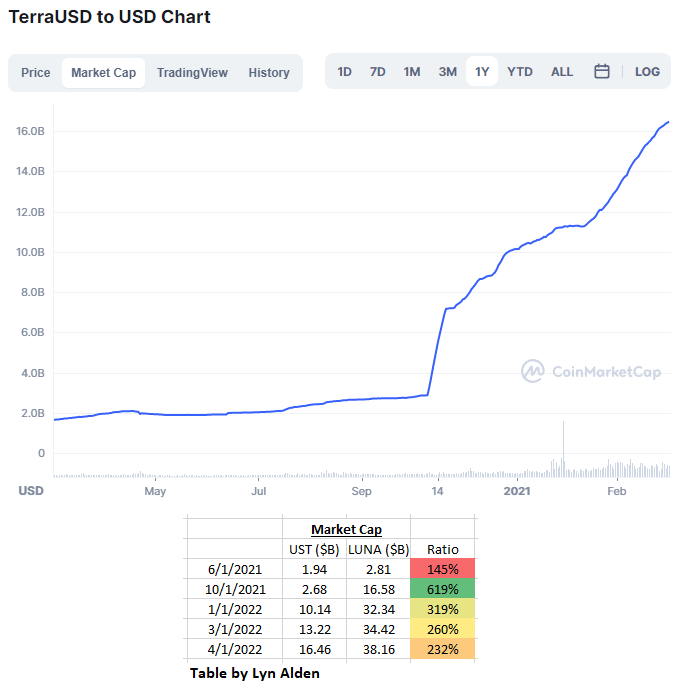

However, if LUNA’s price does not keep pace with UST market cap expansion, then UST can become less and less “backed” by LUNA over time. That’s a general trend we’ve been seeing since late 2021 when UST demand started to take off. At this time, it’s still over 200% backed, but declining fast.

Coin Market Cap, Lyn Alden

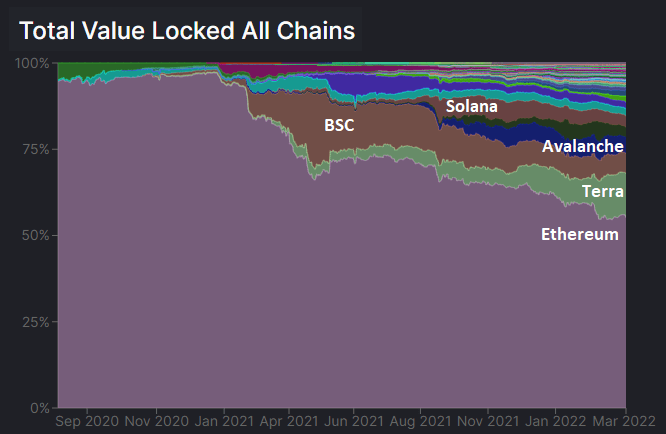

Terra is now the second biggest ecosystem in DeFi based on total value locked:

Defi Llama

The catch? Well, the huge demand for UST is almost entirely driven by unsustainably high yield farming opportunities, much like other DeFi ecosystems. Investors have been able to earn nearly 20% yields on UST in Terra’s Anchor protocol due to various arbitrage opportunities, and that looks like it is starting to dry up. If that VC-supported yield opportunity dries up, UST demand will likely decline. If UST demand shrinks, it could cause a negative feedback loop and liquidity problems for both UST and LUNA, also known as a “death spiral” where tons of capital pulls out of the Terra ecosystem, which crashes the price of LUNA and then eventually breaks the UST peg. If that occurs, it’s functionally very similar to an emerging market currency crisis.

Unlike bitcoin which has no centralized foundation for it, most smart contract blockchains have specific for-profit or nonprofit organizations that serve as their central promotion and development hubs. Terra has Terraform Labs. Solana has the Solana Foundation. Ethereum has the Ethereum Foundation. Avalanche has Ava Labs. These are generally founder/VC-supported entities, with specific leaders and employees trying to promote and develop their ecosystems, and they often use token pre-mines as starter capital.

Terraform Labs and other parties raised capital to set up the Luna Foundation Guard, which will act as a second layer of defense for the UST/USD algorithmic peg rather than that peg relying entirely on LUNA. As they describe it:

“In connection with its stewardship and support of the Terra ecosystem in general, LFG is establishing a decentralized UST Reserve protocol – a non-profit initiative to provide a further layer of support to ensure that UST maintains its peg. In an event where the market price of UST materially deviates from the USD peg, holders of UST will be able to close the arbitrage and bring the market price of UST back to the peg by swapping UST for major, non-correlated assets like BTC that capitalize the reserve. The reserve functions as a release valve for swelling pressure to exit UST to LUNA on-chain, dampening the reflexivity of the system by reducing the dilution of the LUNA supply during severe contractions and restoring the peg in real-time and maintaining an alternative arbitrage opportunity outside of the Terra protocol itself.”

– LFG

One way to think of this is that it’s similar to a country’s sovereign reserve. During good times, an emerging market can use accumulated trade surpluses or currency sales to increase its reserves of foreign assets, such as gold or dollars or euros. Then, if the country later experiences a recession and currency crisis, it can defend the value of its currency by selling some of those reserves that it previously stockpiled, and using the proceeds of those sales to buy back some of its currency units from those that are selling it.

On one hand, Terra buying a lot of bitcoin is bullish for bitcoin… at first. LFG could have bought USDC or USDT as reserves. They could have bought ETH as reserves. They could have bought a mix of these assets as reserves. But instead, they bought BTC as reserves, having judged that to be the best one for the purpose of holding perpetual, decentralized, pristine collateral with minimal counterparty risk. This further validates the argument that bitcoin is the best digital reserve asset. And now, the bigger the Terra ecosystem gets, the more demand they expect to have for their BTC reserve. Eventually as they expand onto other platforms, they intend to add small amounts of other tokens as reserves. For example, to the extent that they expand usage of UST into Solana’s ecosystem, they expect to bring some SOL into their reserves. Their stated expectation is to have BTC be the primary reserve asset along with LUNA, and smaller allocations to other tokens.

On the other hand, this presents a future risk for the bitcoin price. If Terra encounters a problem and is forced to sell a lot of bitcoin to defend its UST peg, it will be detrimental to price in a similar way that their current buying is favorable to the price. Terra’s unsustainable Anchor protocol with 20% yields results in a lot of UST demand, and with this new reserve practice by Terra, UST demand now results in BTC demand. This can be thought of as a source of indirect, artificial, or unsustainable BTC demand, which should eventually dry up. Active bitcoin traders should keep an eye on Terra’s LUNA and BTC reserves relative to UST market capitalization because if it starts to break down and they are forced to defend the UST peg, we could see tens of thousands of coins worth of rapid BTC selling pressure. I’m not saying that will happen but it’s a new factor to monitor going forward.

– Lyn Alden, April 3rd, 2022

I then continued to monitor it, with increasing levels of risk assessment. Here was the segment in my May 1st Stock Waves report:

Luna Note

Back in my April 3rd premium report, I discussed the programming of TerraUSD or “UST” and shared a number of concerns.

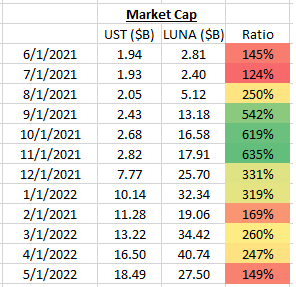

As an update a month later, the market cap of UST increased while the market cap of LUNA decreased, so the collateralization is getting worse:

Lyn Alden

This is not collateralization the same way as DAI is. It’s an algorithmic stablecoin rather than a crypto-collateralized stablecoin. However, the market value of LUNA is an important variable in the long-term integrity of UST.

Their reserve holdings of BTC and AVAX add less than 10% to their total collateralization, so even factoring those reserve assets in, the ratio has been weakening somewhat.

Meanwhile, the Anchor reserve that funds the artificially high yields on UST decreased by 40% in April. This decline represents too many depositors earning a high yield. Eventually, the founders will either need to inject more capital into it (which they did before), or they’ll have to let yields settle to a market rate, which would likely reduce demand for UST.

Mirror Tracker

We’re at a stage where it’s worth paying attention to Terra’s UST peg pretty closely in the months ahead. As LUNA has dropped in value, the amount of collateralization that LUNA provides in order to algorithmically support the UST peg has diminished. This could be salvaged for a period of time by a broad crypto rally, but either way, I’d keep an eye on it here. Meanwhile, the direction of their reserves continues to diminish.

The worst-case scenario is that UST starts to de-peg, and the Luna Defense Guard is forced to sell some or all of their $1.6 billion bitcoin stack into an already-weak market in order to defend that UST peg. I think the way it would work is that UST holders would be able to exchange for bitcoin, at which point many of them would choose to liquidate their position and get back to cash. The Terra network would be severely impaired by that point, and bitcoin would likely take a noticeable price hit.

I would be a buyer of bitcoin in such a capitulation, but it would likely be messy if/when it occurs. That could potentially even mark the bottom of this cycle, with a lot of forced liquidations, similar to Q4 2018 or Q1 2020. I’m not saying it will certainly happen this cycle, but it’s enough of a risk that I’m watching it somewhat regularly now.

Overall, the only investable asset I see across the digital asset ecosystem is bitcoin, but even that is best paired with some cash for rebalancing and volatility reduction in this challenging macro environment. Everything else in the industry is something I categorize as a speculation whenever I analyze it (at best), or basically a ponzi scheme (at worst), depending on the specific asset in question.

– Lyn Alden, May 1st, 2022

Although I was increasingly concerned about it happening, I would not have guessed that Terra would collapse just a week after that second report. These sorts of things can last quite a while if they are backed by a lot of big money funds like Terra was, so I didn’t know when or how it would fail specifically.

Coin Market Cap

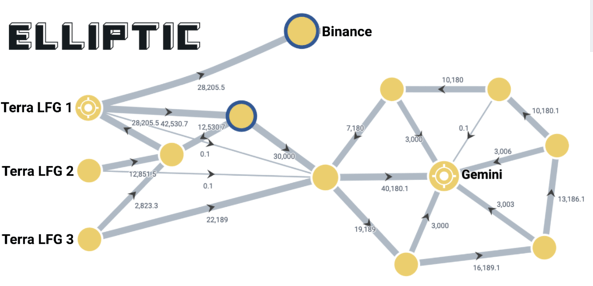

They didn’t even have time to get their automated bitcoin redemption mechanism set up, and so the Luna Foundation Guard was manually and centrally lending their bitcoin reserves to market makers to try to defend the failing TerraUSD peg.

The Luna Foundation Guard’s bitcoin multi-signature address was drained and big inputs showed up on exchanges. It’s currently unclear what the full chain of custody for their bitcoin was, but they sold the vast majority of it and the blockchain analytics firm Elliptic tracked it going to Binance and Gemini:

Elliptic

Evidence suggests that it was a well-funded attack that affected the timing of the Terra/Luna unravel; a large entity apparently sold bitcoin short and went after the TerraUSD peg, right along the lines of how people described that the protocol could be attacked back in 2021. For macro investors, think of it like George Soros going after the Bank of England.

Blaming the attacker misses the point; if something in markets can be successfully attacked, it eventually will be successfully attacked. Algorithmic stablecoins have had a bad track record of failure, and this was the biggest one yet. Since most of their adjustment mechanism was public knowledge, an attacker could know all the specific ways in which to strike it.

Contagion from the collapse of Terra began spreading throughout the digital asset ecosystem. Many VCs had exposure to Luna coins. Thousands of altcoins began to bleed out. Various pools of capital were frightened out of the space. It’s a period of broad re-evaluation across the ecosystem, to separate the wheat from the chaff. Most of it is chaff.

Bitcoin itself continues to function with no permanent impairment other than a price hit, while the Terra ecosystem received a kill shot, and the broad cryptocurrency industry is somewhat maimed from a regulatory, reputational, and liquidity standpoint.

Summary Thoughts

I remain structurally bullish on bitcoin as part of a portfolio, especially with recurring purchases over time to take advantage of the volatility.

Although there are risks to the view, I think this year 2022 will be looked back on as a good time for accumulation for investors with a 3-5 year view, similar to the year 2020, year 2018, and the year 2015 capitulations.

Look Into Bitcoin

While there are other neat blockchains out there, there are none that I have personally found to be investable with a decent risk/reward ratio. Investors should use considerable caution when speculating on any crypto token outside of bitcoin, if they do so at all. Even for bitcoin, investors must maintain appropriate position sizes relative to their tolerance for volatility and assessment of its network risks.

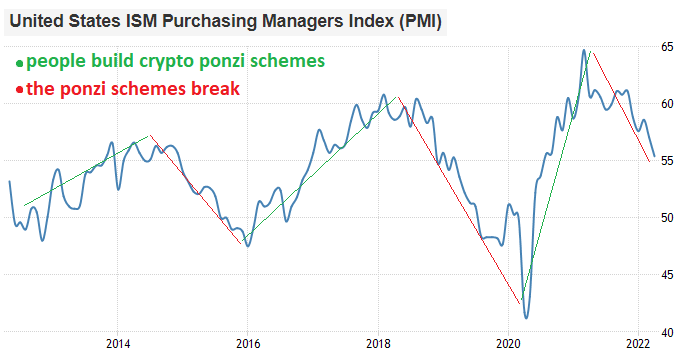

I view the ongoing monetization of bitcoin similar to a bodybuilder’s bulking and cutting cycle. Bodybuilders often focus on revolving cycles of mass creation followed by fat reduction, so that after numerous cycles they accumulate a lot of muscle while avoiding fat accumulation.

During bull markets, bitcoin goes up in price but faces dilution from thousands of new projects, like building muscle and fat at the same time as part of the mass-creation cycle. When liquidity is flowing, anyone with an idea can get funding and can pull investors in with promising narratives. Outside capital flows into bitcoin, but then it begins getting distracted by these shiny new objects and begins diluting into all of these other things.

And then during the bear markets, liquidity flows out. Bitcoin takes a price hit, but the thousands of altcoins take a much bigger price hit. Excessive debt is destroyed, pegs are broken, Ponzi schemes are laid bare, and weak networks are ripped apart. Crypto muscle growth comes to a halt and even shrinks some, but importantly large swaths of unproductive crypto fat is burned away, so that the next growth cycle can begin anew.

Trading Economics

When each new cycle comes, bitcoin’s network effect and investment thesis have historically remained intact, while most other projects become stagnant and discarded by developers and investors. Bitcoin has gone on to make higher highs in four separate major cycles, with greater levels of adoption and development each time, while the majority of altcoins only go through one or two cycles before rolling over for good.

Even many of the most notable coins eventually stagnate. If we look at the top 10 coins near the end of the 2017 bull market, for example, every single one of them went on to underperform bitcoin from those highs in the subsequent bear market and bull market. ETH, BCH, XRP, LTC, ADA, MIOTA, DASH, NEM, and XMR all reached lower highs as denominated in BTC during the 2021 bull run compared to the 2017 bull run.

Coin Market Cap

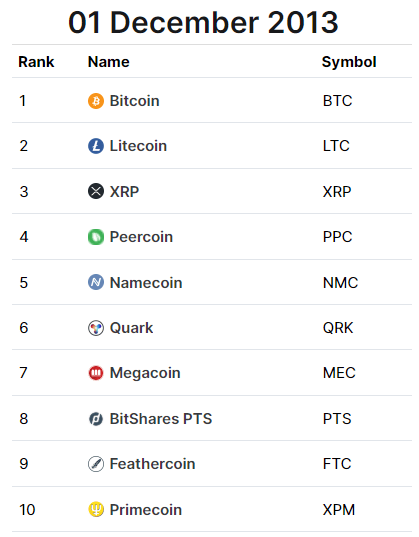

The same is basically true if we look back to the 2013 bull run as well; people today haven’t even heard of most of those top ten coins by now. Of this list, only XRP went on to make higher highs in 2017 as denominated in BTC compared to 2013, but then it failed to do so in the 2021 cycle. None of the others managed even one more cycle of bigger BTC-denominated gains.

Coin Market Cap

I think this pattern will continue; there’s a high probability that most of the crypto darlings of the 2021 bull run have already seen their all-time highs as denominated in BTC. Maybe one or two will go on to get a higher high at some point, but most will not.

That doesn’t mean that bitcoin is without risks, but it has by far the best track record in the space and is the one designed with a specific purpose in mind. Block after block, it continues to operate as intended over time.