“We think the best approach is not to clamp down or ban these things,” said Ravi Menon , managing director of the Monetary Authority of Singapore.

The president of El Salvador is currently in Turkey , the first G20 country to experience near hyperinflation. I would guess Nayib Bukele would bring up the benefits that adopting bitcoin as legal tender could do for the Turkish people.

For every case like China, which chose to close its doors to Bitcoin, there are two other countries ready to embrace it. You cannot ban Bitcoin, a country can only choose to ignore it, but Bitcoin is not going away. Ignore at your peril. Bulgaria owns 213,518 bitcoin, Ukraine owns 46,351, Finland 1,981 and El Salvador, at the time of writing, 1,220.

Even in countries where governments do not present favorable policies toward Bitcoin adoption, high levels of citizen adoption can force the government’s hand. Nigeria and Turkey are two prime examples. Grassroots citizen adoption (retail) is taking hold in countries all over the world. In 2020, per the Statista global survey, 32% of citizens in Nigeria, 21% in Vietnam, 20% in the Philippines and 16% in Turkey and Peru have indicated they have used or owned “cryptocurrencies.”

Corporate accumulation is also taking place. As of June 2021, 34 public companies collectively hold over 213,000 bitcoin. MicroStrategy and Tesla being the largest. The majority of companies who have adopted bitcoin have done so in the last 18 months.

Google has partnered with Bakkt to provide Bitcoin payment solutions. Twitter has enabled tipping via the Bitcoin Lightning Network. Bitcoin has the capability of being the native currency of the internet, as predicted by Milton Friedman in 1999.

One of the most prominent U.S. real estate investment trusts (REITS), SL Green Realty Corp. (NYC Office REIT), has dipped their toes into bitcoin with a $10 million investment in a bitcoin fund. Banks are another corporate sector actively embracing bitcoin after trying to ignore and fight the asset for years. Banks make their money by lending out their assets. The Commonwealth Bank of Australia has enabled 6 million of its customers to buy bitcoin. Banks must choose to adopt bitcoin or risk becoming irrelevant.

Pension funds and insurance companies are also beginning to gain exposure to bitcoin. The Houston Firefighters Relief and Retirement Fund (HFRRF) in partnership with NYDIG has purchased $25 million in bitcoin (and ether) in October 2021. MassMutual also purchased $100 million in bitcoin in December 2020.

The reason why pension funds and insurances are drawn to bitcoin is because they need to save their monetary energy (purchasing power) for the future. With inflation levels at decade highs, cash savings (in fiat) are being devalued. These funds are forced to take on riskier investments in search of higher yields, to maintain their purchasing power that is being devalued through inflation.

Holding bitcoin is simpler, as bitcoin enables the ability to save due to its deflationary nature.

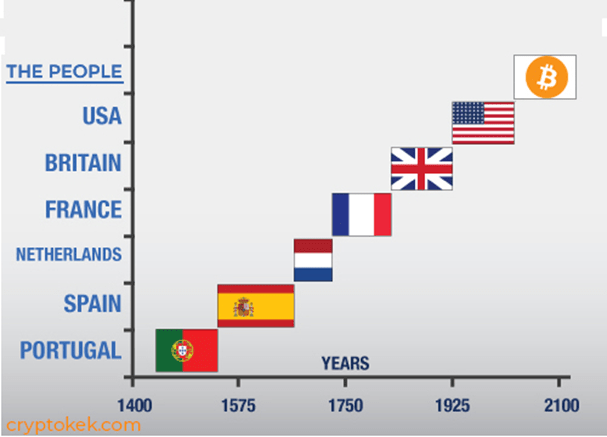

The toothpaste (Bitcoin adoption) can’t go back in the tube. Adoption has grown to a saturation level (in terms of scale and diversity) which makes a future bitcoin standard for the world inevitable. The majority of the world has blinders on and cannot see this or the groundswell of adoption and accumulation taking place.

Paul Tudor Jones says it best, “Bitcoin has this enormous contingent of really, really, smart sophisticated people who believe in it…. You’ve got this group — which by the way is crowdsourced all over the world — that are dedicated to seeing Bitcoin succeed in becoming a commonplace store of value and transactional to boot.”

It might make sense to get some, in the event that the rate of adoption continues to accelerate.

This is a guest post by Drew MacMartin. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.