Since H2 2020, we have seen the meteoric rise of DeFi mainly on Ethereum, and the subsequent boom of CeDeFi through the Binance Smart Chain (BSC). With that, the question of who would end up dominating the market arises: be it Ethereum or BSC, and by extension DeFi or CeDeFi.

While Binance CEO Changpeng Zhao calls for an ‘infinite mindset’ and does not want to frame BSC as a competitor to Ethereum, their markets ultimately overlap, at least partially.

The infinite mindset where both networks see huge growth works for now, given the huge room for growth in the market. After all, a rising tide lifts all boats.

For those bullish on DeFi and its potential to complement and replace some segments of traditional finance, it is evident that both BSC and Ethereum can grow simultaneously — they are not playing a zero-sum game.

Hence, the article is not meant to answer the question of whether BSC will kill Ethereum. It likely would not.

Rather, we focus on identifying and exploring the defensibility of the two players’ competitive advantages/ disadvantages, and how this might shape their market position and dominance over time.

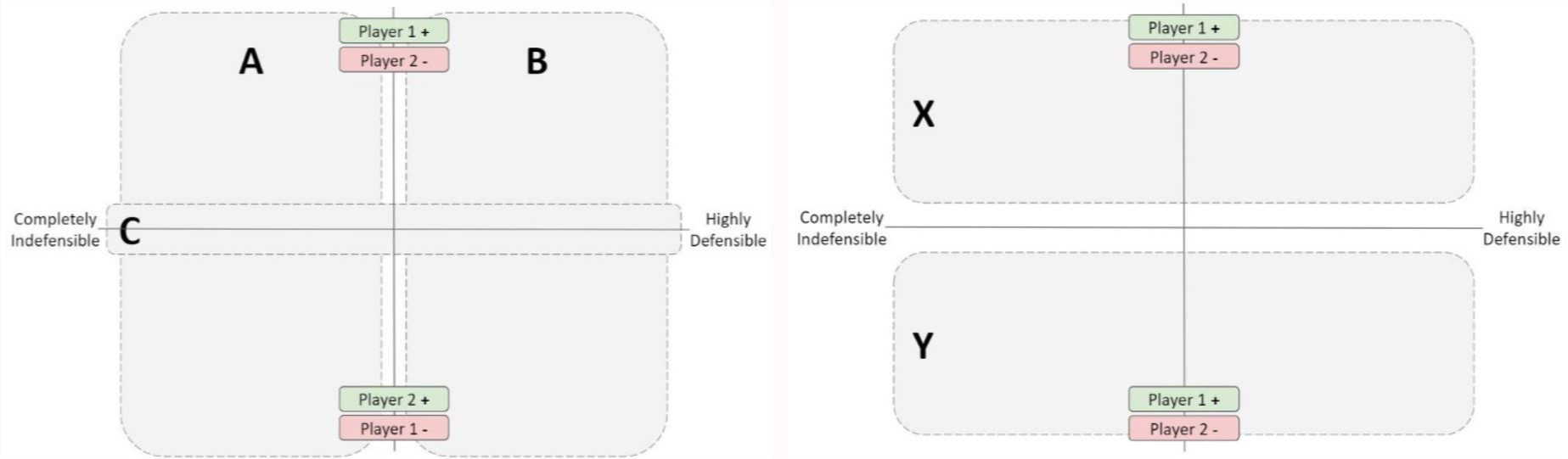

The Competitive Advantage/ Defensibility Map

To better visualize the current market position of Ethereum in relation to BSC and evaluate potential future changes, we introduce the competitive advantage/ defensibility map.

Before filling the map with Ethereum/ BSC specific information, we would explore how to read and analyze it:

- A: factors that can provide short term advantage to either player

- B: factors that can provide long term advantage to either player

- C: potential future areas of competition where neither side currently has a clear advantage in. It can be exploited by either side to outcompete the other

- X & Y: overweight presence of factors (number and significance) in either of these regions compared to the other reflects a stronger “net” competitive advantage of one over the other at the current point in time

It should be noted that the map represents the current state of affairs and the factors (represented by bubbles in the map), may move over time:

- Vertical movement: decisions made by either player (centralized business like Binance or a developer community) can improve a player’s relative performance on a given factor/ metric. Factors on the right of the map (more defensible) are more resistant to vertical movement

- Horizontal movement: such movement is limited given that the extent of a factor’s defensibility is usually intrinsic. However, external forces such as technological advancement could cause changes in defensibility

The rest of the article revolves around filling in and analyzing the implications of this map with respect to Ethereum and BSC.

Ethereum vs BSC: Areas of Competition

1. Extent of decentralization

As a community-driven open-source blockchain with currently about 10,000 independent nodes, Ethereum is unlikely to ever face the third party risk inherent in BSC and CeDeFi. Meanwhile, BSC has 21 nodes elected by Binance Coin (BNB) holders.

As Binance controls a huge amount of BNB, it has significant control over the chain. While Binance is financially incentivized to operate fairly and has a good track record, the control makes it an easy target for regulation and there is a small but present risk that Binance goes rogue.

As an intrinsic property of CeDeFi, this advantage is highly defensible. However, the value of decentralization may be different depending on who you ask and it is currently treated as a philosophy some people adopt but others care little about.

For potential institutional users, the implications of this difference may be more complicated. BSC’s more centralized structure and dependence on Binance could be seen as a risk for institutions that may allocate significant capital in the system.

At the same time, being easier to regulate given its centralized nature, it is possible that BSC may be safer if it gets regulated, as this eliminates regulatory risk.

2. Infrastructure & Network

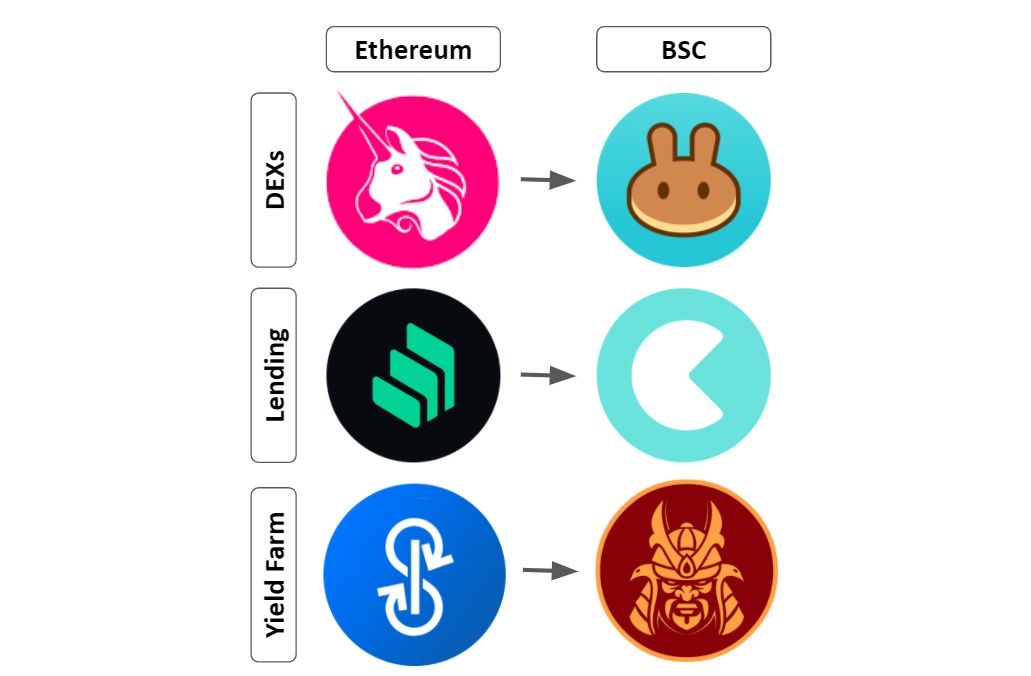

A first-mover in the DeFi space, Ethereum maintains the largest number of DeFi dApps compared to any other blockchain, with most innovation in DeFi happening there. This robust infrastructure has led to a large community of users that provide the liquidity necessary for the functioning of DeFi.

However, BSC’s infrastructure is playing catch up quite well, attracting and building the size of its network in the process. There are two main reasons for this.

Firstly, it is easy to make BSC clones of Ethereum dApps as BSC is EVM (Ethereum Virtual Machine)-compatible.

Secondly, Binance’s $100 million fund has been incentivizing dApp development on BSC.

BSC also rides on Ethereum’s tailwinds, given that Ethereum has already helped to popularize DeFi and educate people about it. This facilitates the rapid adoption of BSC.

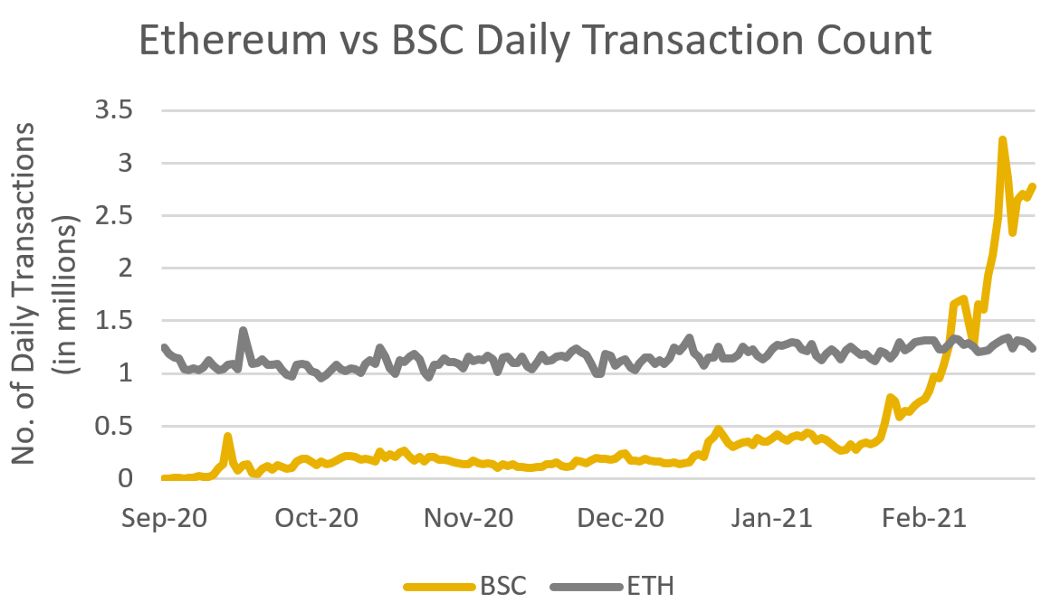

According to DappRadar, BSC has already surpassed Ethereum on the number of daily transactions and daily active users.

The extensiveness of available infrastructure is probably less important for retail users compared to institutional users who may want access to more sophisticated dApps and functionality.

CSV Data obtained from Etherscan and BscScan (Sep 2020 to Feb 2021). Note that this does not account for transaction sizes.

3. Transaction fees and times

Since launch, BSC’s daily average fees have hovered around 20+ Gwei (of lower-priced BNB) while Ethereum’s average fees across February 2021 ranged from 150 to 375 Gwei (of higher-priced ETH). High growth and demand on Ethereum have congested its network, causing high gas prices.

Moreover, BSC runs on a Proof of Staked Authority (PoSA) system compared to Ethereum’s Proof of Work (PoW). On a technical level, this allows BSC to have significantly lower fees and shorter block times.

Ethereum’s high fees prices out many retail users whose small transaction sizes mean that gas account for a significant percentage of the transaction. This greatly reduces the range of actions that make financial sense, preventing participation in DeFi.

For instance, when gas makes up 10% of the transaction, depositing DAI into Compound at a ~10% APY no longer makes sense.

Arguably, low fees have been the main driver of BSC’s popularity, being highly attractive to users with low transaction sizes.

However, it is important to note that gas price is a function of supply and demand. If high gas prices drive away demand, the decreased activity would lower gas prices, reducing the push factor.

Hence, the issue of gas may weaken, but will not kill Ethereum. Also, the rollout of Eth2 with the implementation of sharding and Proof of Stake (PoS) would increase the network’s scalability and reduce BSC’s advantage in this area.

4. User Experience

Currently, interacting with dApps on both Ethereum and BSC is complex, requiring many steps. This acts as a barrier to entry for most given the time it takes to learn and set up.

Interacting with DeFi/ CeDeFi should not require long tutorials, it should be made as intuitive as possible. Possible areas for UX improvement include improving the ease and cost of fiat on/off ramps, providing an aggregator for easy interaction with multiple dApps, reducing the number of steps etc.

Being faster in UX improvement could provide a short-term advantage for either chain, before the other copies the improvement. UX is likely to be more important for retail users as compared to institutional users, who can afford to have an expert employed to navigate the ecosystem even if the UX is poor.

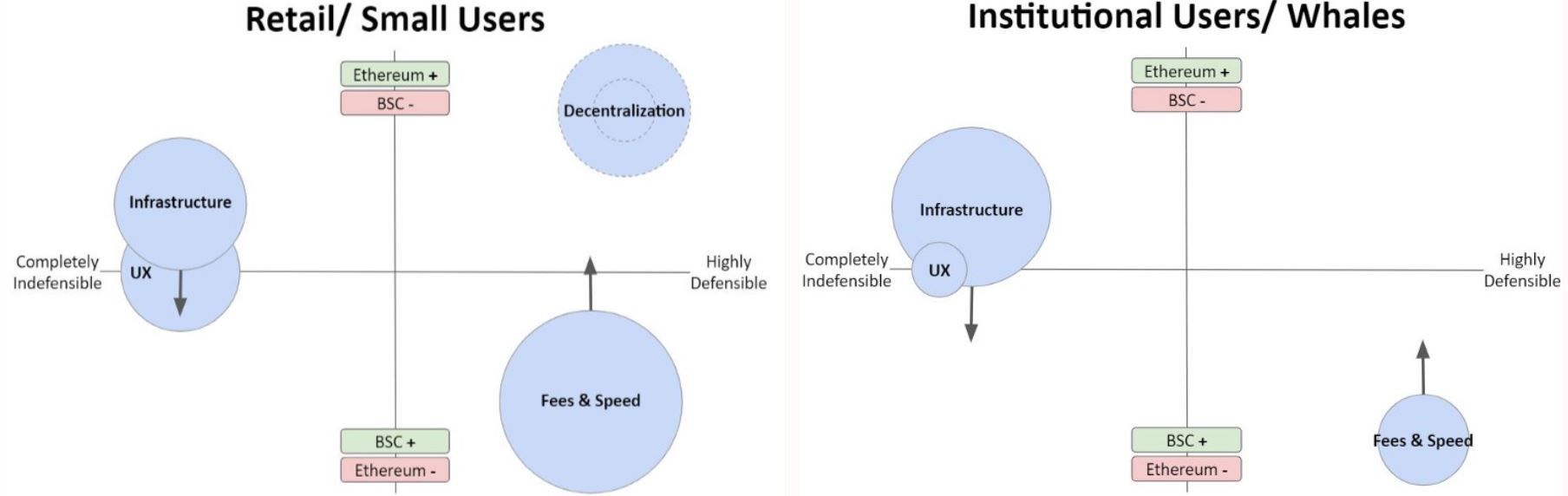

The Future of Ethereum vs BSC: Analysing the Map

Here, we have plotted the 4 factors explored in the previous section on the map, with different bubble sizes indicating the importance of the factor and arrows indicating the expected movement over time (remember that factors on right are more resistant to vertical movement).

Decentralization is not included in the institutional users’ map given the complexity discussed in the previous section.

Based on the above maps, we may now make an educated guess on how Ethereum and BSC’s market position may evolve over time:

1. Short-term

In the short to medium-term, traditional institutional players are unlikely to participate in either ecosystem due to high regulatory uncertainty and risk. As a newer platform, BSC is likely to continue to see stronger percentage growth relative to Ethereum in the short term.

Small retail users of Ethereum disgruntled by high gas fees would likely participate in BSC, and new retail users entering the space are likely to prefer BSC over Ethereum for the same reason.

BSC’s dApp diversity and infrastructure would continue to improve as more Ethereum dApps are cloned. Meanwhile, Ethereum would be anchored by large retail users (whales), and small users who are hardcore believers in decentralization.

2. Medium-term

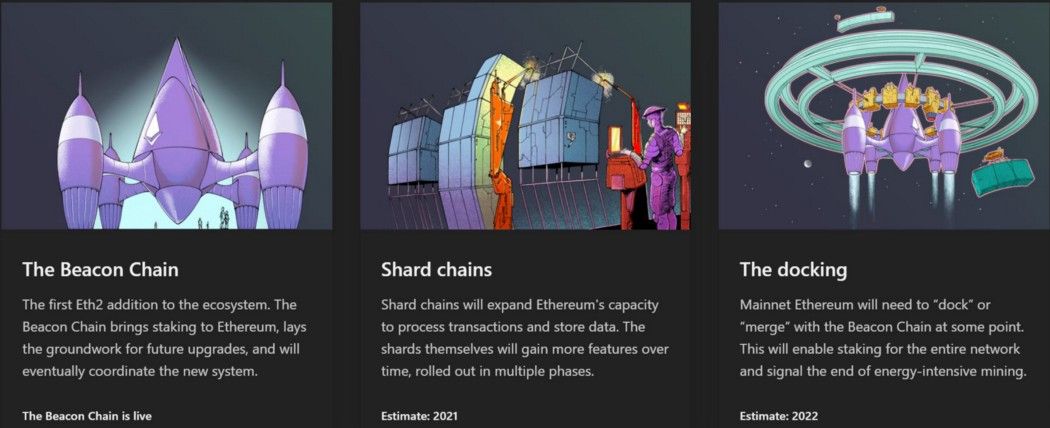

As Eth2 gets rolled out and is eventually incorporated into Mainnet, BSC’s main advantage of lower costs becomes comparatively less impressive. New users join both BSC and Ethereum in an even manner as neither has a significant advantage over the other.

Eth2 rollout timeline taken from Ethereum.org

For users, Ethereum is attractive for its decentralization and brand as the first mover. Meanwhile, BSC has the advantage of easily luring new users just getting into crypto through its Binance platform, given the platform’s integration with BSC.

Some retail users who have previously shifted to BSC due to price may increase their activity on Ethereum again.

The developer community’s interest in BSC matures, and new innovative projects may happen on BSC alongside Ethereum. However, Ethereum’s stronger brand among developers would likely mean that most innovation still happens on Ethereum first, but is quickly cloned to BSC.

Their dApp availability and infrastructure are thus likely to be at similar levels.

3. Long-term

Traditional institutional players enter the space. If regulation is equally certain/ uncertain on both Ethereum and BSC (DeFi and CeDeFi), Ethereum may be preferred due to its decentralized nature which reduces the risk associated with excessive dependence on a single party (Binance). Moreover, institutions would probably join as builders besides being users.

With that, Ethereum may ride the institutional wave to market dominance. Nevertheless, BSC is likely to continue on with significant market share, remaining as a leader in the matured DeFi/ CeDeFi market.

Closing Thoughts: Alternative futures

While we have focused on Ethereum vs BSC, they may not necessarily be the two sole dominant players of the future. Nevertheless, a number of points in this article are applicable to the larger DeFi vs CeDeFi debate.

The future may play out in a number of other ways:

- Multi-chain future: multiple projects/ chains gain significant market share within both DeFi (eg. Polkadot, EOS) and CeDeFi (CeFi exchange OKEx is working in this space and other large CeFi players may do something similar to BSC given its success) alongside Ethereum and BSC.

- The Ethereum Bear Case: Eth2’s slow rollout may be indicative of Ethereum’s Achilles heel: slow innovation in Layer 1 and 2. While Ethereum has enjoyed great innovation in Layer 3 with dApps that attract users, this may cease to be the case if Layer 1 and 2 can’t accommodate them well. This may introduce a multi-chain future where Ethereum is a small player alongside more scalable chains, a well-remembered giant fallen from grace.

- CeFi directly integrates DeFi: CeFi players could allow users to access DeFi protocols (eg. Ethereum dApps) through their platform. This is different from Binance’s approach of creating its own smart chain and CeDeFi ecosystem from the ground up. The approach may be preferred by smaller CEXs who lack the resources to build something like BSC and who wish to overcome the competitive disadvantage of being unable to provide their users with the benefits of a CeDeFi ecosystem. Some CeFi players have started doing so, such as OKEx and Coinbase which offer interest on stable coin DAI (with Dai Savings Rate likely at the backend of this).

- DeFi/ CeDeFi remains small: while I personally hope for and am bullish on the industry’s growth, there is a possibility that DeFi/ CeDeFi never goes mainstream. As a new innovative space, there is also significant regulatory uncertainty surrounding it.

Regardless of what happens, it is captivating to watch (and participate in) this space as the future unfolds.

I try to share thoughtful content and maximize signal:noise ratio. Catch me on the following platforms: linktr.ee/gideon.tay.

Read behind a paywall here