Coinbase, the largest U.S. bitcoin and cryptocurrency exchange, has had a hard time lately.

Repeated outages at the exchange have left many users locked out of their accounts just as the bitcoin price made major moves.

Now, following reports Coinbase will soon begin selling blockchain analysis software to the U.S. government, its users are withdrawing bitcoin and looking for alternatives.

The San Fransico-based bitcoin and cryptocurrency exchange Coinbase has seen a backlash from users … [+]

“If you use Coinbase you should delete your account,” bitcoin and crypto entrepreneur Matt Odell said after The Block reported the U.S. Drug Enforcement Administration (DEA) and the Internal Revenue Service (IRS) intend to buy licenses from Coinbase for an analytics platform called Coinbase Analytics.

Other influential voices in the bitcoin and crypto community echoed Odell, asking if Coinbase customers could trust the exchange to keep their data private.

The San Francisco-based exchange hit back, promising the blockchain analytics tool, built off its acquisition of blockchain data firm Neutrino in late 2019, “does not include any personally-identifiable information for anyone, regardless of whether or not they use Coinbase.”

Coinbase “offers this product to financial institutions and law enforcement agencies to support compliance and investigation use cases,” a company spokesperson said.

“This tool only offers them streamlined access to publicly-available data and at no point do they have access to any Coinbase internal or customer data.”

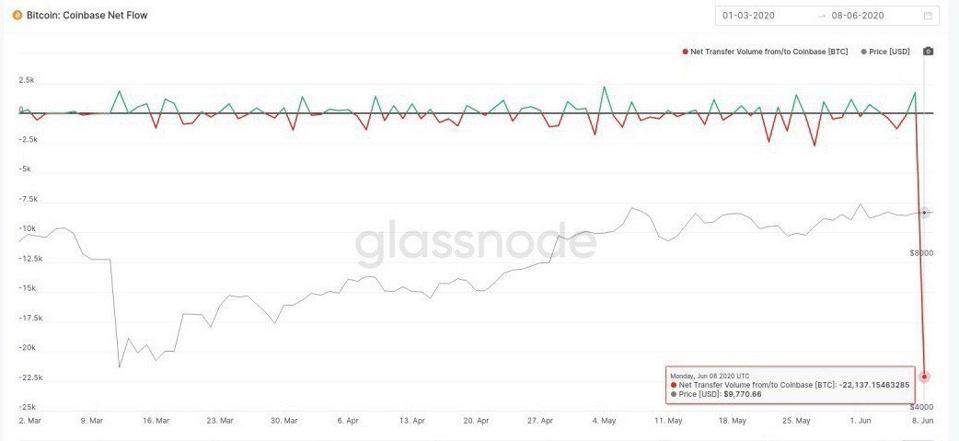

These security concerns and recent outages have caused Coinbase customers to withdraw a near-record amount of bitcoin from the exchange, according to data from blockchain analytics firm Glassnode.

Coinbase users withdrew 22,000 more bitcoin (worth $214 million) than they deposited on June 7, two days after the Coinbase Analytics story broke and a week after the exchange’s latest outage.

Users of the Coinbase bitcoin and cryptocurrency exchange have withdrawn a record number of bitcoin … [+]

Coinbase blamed the June 1 outage on a five-fold traffic spike that caused the exchange’s servers to buckle after they were “unable to keep pace with this dramatic increase in traffic.”

The coronavirus pandemic and subsequent lockdowns have caused bitcoin exchange volumes to soar along with traditional markets in recent months.

“The crypto markets have experienced much of the same unprecedented volatility and activity during the outbreak the traditional markets have, which means the underlying tech infrastructure has effectively been stress tested daily,” said Jim Nevotti, president at trading software provider Sterling Trading Tech, adding “even seconds of downtime to switch platforms can have an impact during volatile periods.”

Elsewhere, a Twitter poll of 5,000 people carried out by bitcoin and crypto trader Josh Rager at the end of last week showed two-thirds of people who use Coinbase are willing to leave the platform.