Introduction

Options become a hot topic in crypto. Volumes are skyrocketing on Deribit and new initiatives have flourished in the DeFi ecosystem.

But did you know you can generate a nice yield with options?

Today we explain one basic strategy: Covered calls.

For those with no knowledge on options, we advise you to read our first article dedicated to strategies to short ETH via futures or options, here. We explain briefly what are options with few examples.

ETH Covered calls

A covered call is an option strategy where you are required to hold the underlying asset (ETH-USD) on which you will sell (write) call options. You are selling insurance on your ETH holdings that the price of ETH will not go higher than the strike price.

It is a strategy to generate income with your spot ETH holdings.

Imagine you hold spot ETH and you don’t want to sell it ( you are a true hodler). Instead of praying the Ethereum God to make it moon ASAP, you could just use your brain and make money out of it, right now.

Imagine you could sell your ETH for a higher price in the future?

Covered calls is the way to go.

Requirements and example:

Let’s explain the strategy.

-

You hold 100 ETH at $234, meaning you have assets valued at $23,400 USD.

-

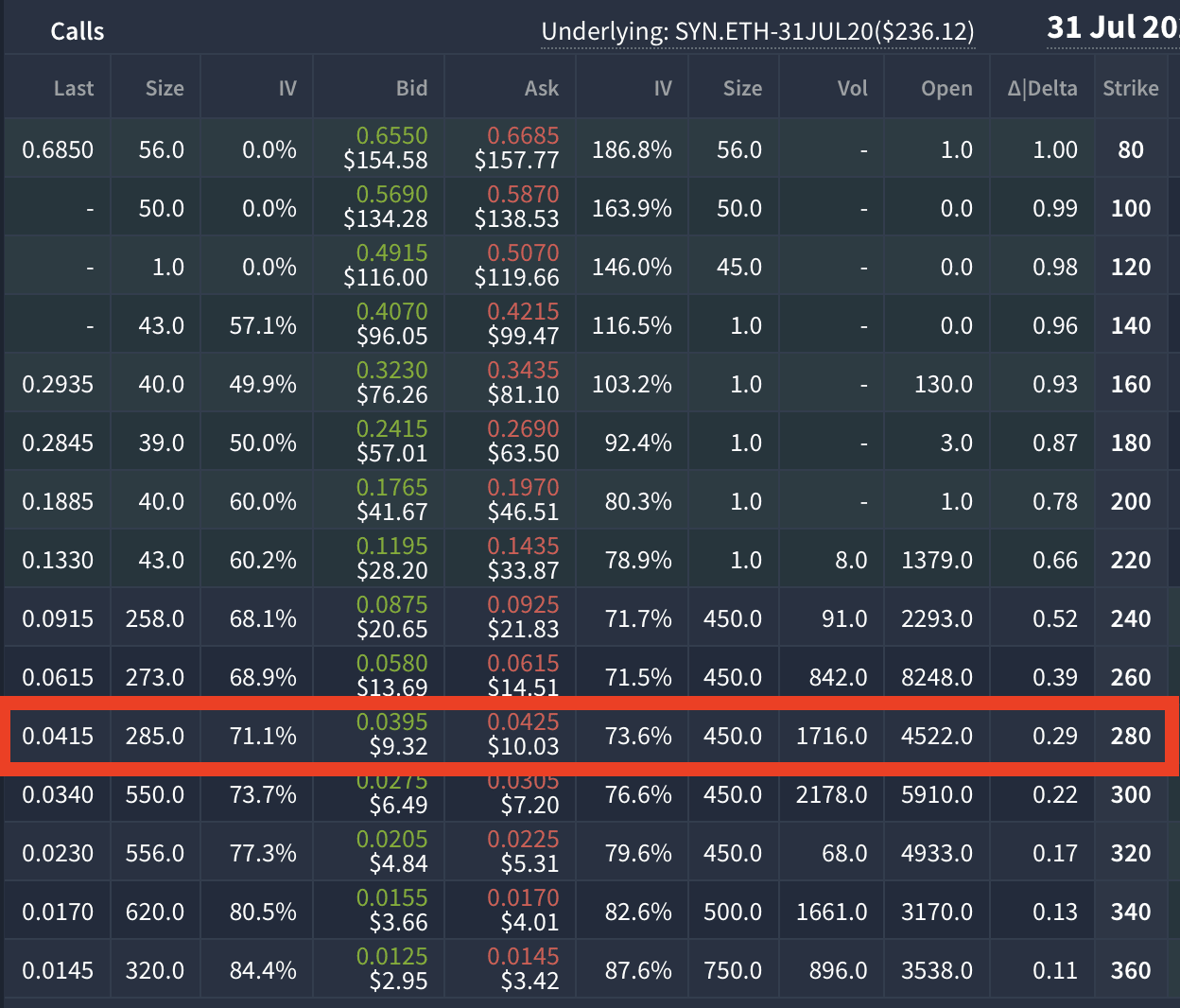

You sell 100 call option contracts with expiry date on 31 July 2020 and a strike price at $280. Taking the bid price, you earn a premium of $932, upfront.

-

You hold your ETH and your calls until expiry.

{kind=link}

-

At the expiry date (31 July 2020), you keep the premium earned if ETH does not finished above $280 at the expiry date. If ETH goes higher than $280 + the premium paid per call option (in this example, $9.32) so a price higher than $289.32, you will “lose” opportunity to make more money by having not sell call options as ETH price went up a lot.

4 possible outputs

There are 4 different outputs at the expiry date, which are described below.

We then compare the results from selling covered calls on ETH to a simple strategy of holding ETH (without any options) to demonstrate why covered calls are interesting for your portfolio if you are willing to take some time to learn how to do it.

As we always say, there is no free lunch. So to make additional return with covered calls, risks and opportunity cost shall be explained.

We define for scenarios at the expiry date:

-

ETH is at $300 at expiry date

-

ETH increases by 10% and is trading at $257 at expiry date

-

ETH did not move and is trading at $234 at expiry date

-

ETH went south to $200 at expiry date

#1 – ETH is at $300 at expiry date

In this case you will “lose” money on your calls sold. But actually, you do not lose any money as you had spot ETH bought at $234. Let me explain.

You are only losing opportunity to sell ETH at a higher price than $289.32 (strike price + premium paid per call).

Your counterparty will use its right to exercise the call options at $280 because the market price is higher than the strike price, so you will give him your ETH at $280.

Quick math:

-

At trade initiation, you had $23,400 USD worth of ETH (100 ETH at $234) and the premium collected ($932), so a total of $24,332 USD.

-

On expiry date, you will have to sell your ETH holdings to your counterparty at $280 per ETH (the strike price), so your spot holdings are sold for $28,000 USD and you still keep your premium, for a total capital of $28,932 USD, or a return of 23.6% in 45 days.

If you had not sold any call options, you had only kept your 100 ETH. you would have a total capital of $30,000 USD, or a return of 28.2%.

Outcome:

Simple holding of ETH provides a higher return: you do not have to encounter the opportunity cost of selling covered calls.

#2 – ETH increases by 10% and is trading at $257

In this case, the price at expiry is below the strike price so your counterparty does not exercise his calls and loses the premium paid.

Quick math:

-

At trade initiation, you had $23,400 USD worth of ETH (100 ETH at $234) and the premium collected ($932), so a total of $24,332 USD.

-

On expiry date, ETH is at $257 so below the strike price of your calls, so your counterparty does not exercise. Why doesn’t he exercise? Simply because he can buy ETH at $257 in the market so why exercise something at $280 (it does not make any sense).

The option you sold is now worthless and you keep the premium collected.

You have a capital of $25,700 (100 ETH at $257) + the premium collected ($932), so a total capital of $26,632, or a return of 13.8%.

If you had not sold any call options and had only kept your 100 ETH, you would have a total capital of $25,700 USD, or a return of 9.8%.

Outcome:

Covered calls earn a higher return thanks to the premium collected.

#3 – ETH did not move and is still trading at $234 at expiry

Again, the price at expiry is below the strike price so your counterparty does not exercise his calls and loses the premium paid.

-

At trade initiation, you had $23,400 USD worth of ETH (100 ETH at $234) and the premium collected ($932), so a total of $24,332 USD.

-

On expiry date, ETH is at $234 so below the strike price of your calls, so your counterparty does not exercise. Why doesn’t he exercise? Simply because he can buy ETH at $234 in the market so why exercise something at $280 (it does not make any sense).

The option you sold is now worthless and you keep the premium collected.

You have a capital of $23,400 (100 ETH at $234) + the premium collected ($932), so you have a total capital of $24,332, or a return of 3.9% for 45 days. Annualised is a whopping 37% return.

If you had not sold any call options and had only kept your 100 ETH, you would have a total capital of $23,400 USD, or a return of 0%.

Outcome:

Once again, covered calls earn a higher return thanks to the premium collected.

#4 – ETH tumbles to $200 at expiry date

Again, the price at expiry is below the strike price so your counterparty does not exercise his calls and loses the premium paid.

-

At trade initiation, you had $23,400 USD worth of ETH (100 ETH at $234) and the premium collected ($932), so a total of $24,332 USD.

-

On expiry date, ETH is at $200, your counterparty does not exercise as market price < strike price.

The option you sold is now worthless and you keep the premium collected but ETH price is down so your capital is down as well.

You have a capital of $20,000 (100 ETH at $200) + the premium collected ($932), so you have a total capital of $20,932, or a negative return of -10.5%.

If you had not sold any call options and had only kept your 100 ETH, you would have a total capital of $20,00 USD, or a negative return of -14.5%.

Outcome:

Covered calls also provide a small protection against downside as you keep the premium.

Key takeaways

Covered calls is an option strategy used to generate income on the positions you hold. You make your assets work for you and you generate a yield. You are not taking additional risk by doing that as you hold the underlying asset. Never write naked calls (selling calls when you do not hold the underlying asset because it is a very risky strategy (limited return and unlimited downside) and shall only be done by professional investors.

As there is no free lunch in this world, covered calls come also with one drawback: you cap your upside to the strike price of the call option sold. That’s why we do not advise to sell long term call options on Crypto assets. You never know where ETH or BTC are going to be in a year.

In our humble opinion, selling monthly covered calls is the ideal strategy. You generates additional yield and cap your upside to the strike price. We would rather take a monthly yield of 5% guaranteed by selling covered calls and in the best case scenario (where ETH would go up a lot) take an additional 20% than awaiting an hypothetic +50% in a month. You get the idea.

Thanks for reading

Secret Salsa

Disclosure: I am/we are long ETH-USD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.